IRA Planning & Distribution Guidance

Make More Informed Decisions About Your Retirement Accounts

For many retirees, IRAs and retirement accounts represent a significant portion of their savings. The challenge isn’t simply building those accounts—it’s knowing how and when to use them.

The timing of withdrawals can affect taxes, Social Security benefits, Medicare premiums, and the amount of money available to support your lifestyle in retirement. A thoughtful distribution strategy can help you understand your options and avoid costly surprises later.

At Safe Harbor Wealth Management, we help individuals and families throughout Ocean County, Monmouth County, and New Jersey develop strategies for managing IRA withdrawals, Required Minimum Distributions (RMDs), and retirement account income as part of a larger retirement plan.

Looking Beyond Required Minimum Distributions

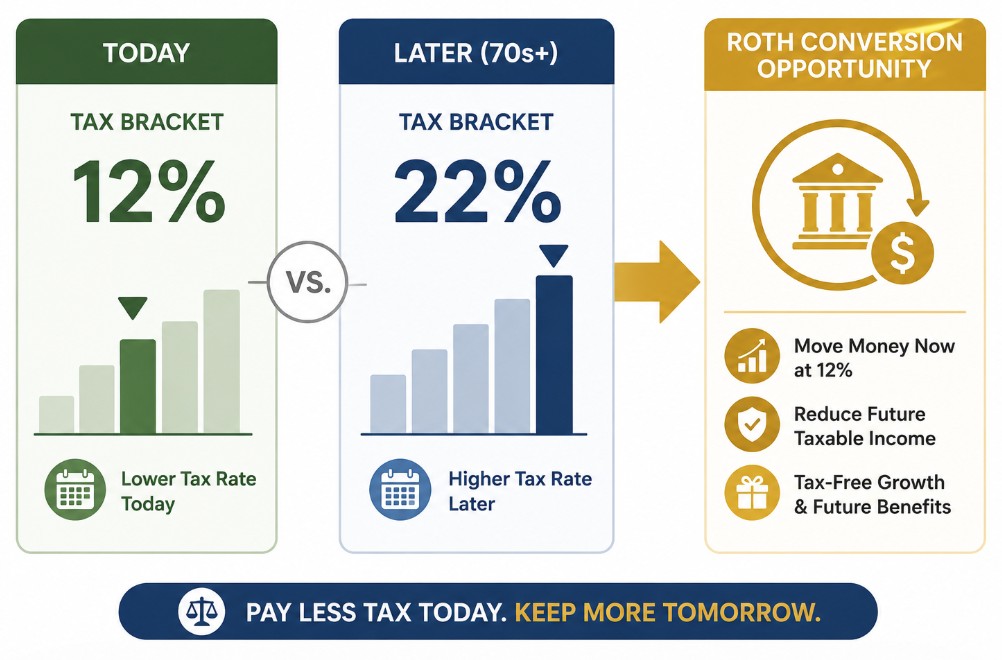

Many retirees are surprised to learn that their tax burden can actually increase later in retirement.

Once Required Minimum Distributions begin, larger IRA balances can create substantial taxable income. Combined with Social Security benefits and other income sources, these mandatory withdrawals may push retirees into higher tax brackets than they anticipated.

That’s why we often encourage clients to look beyond today’s tax return and evaluate what their tax situation may look like in their 70s and beyond. Sometimes, taking strategic action earlier can create opportunities later.

The Opportunity to Manage Future Taxes

One strategy we frequently evaluate is what Chad refers to as “bumping the bracket.” In some situations, retirees may currently be in a relatively low tax bracket. Rather than waiting for larger Required Minimum Distributions to force higher taxable income later, it may make sense to strategically withdraw or convert portions of retirement assets while taxes are lower.

For some individuals, this can mean:

- Reducing future Required Minimum Distributions

- Creating opportunities for Roth conversions

- Building tax diversification

- Managing future tax exposure

- Increasing flexibility later in retirement

Every situation is different, which is why personalized analysis is essential before implementing any strategy.

For illustrative purposes only. No specific investments were used in this example. Investments are subject to risk, including the loss of principal. Actual results will vary.

Common IRA Distribution Questions

Create a Distribution Strategy That Works for You

The goal isn’t simply taking money out of retirement accounts. It’s understanding how withdrawals fit into your broader retirement income, tax, and legacy planning strategy.

At Safe Harbor Wealth Management, we help clients evaluate their options, understand potential tax consequences, and create retirement account distribution strategies designed around their goals.